Introduction

When creating an SPV, one of the first decisions to make is how to structure fees. The two main options are carried interest (typically referred to as carry), a percentage of the profits when the investment pays off, and a management fee, a flat annual charge paid by investors regardless of outcome.

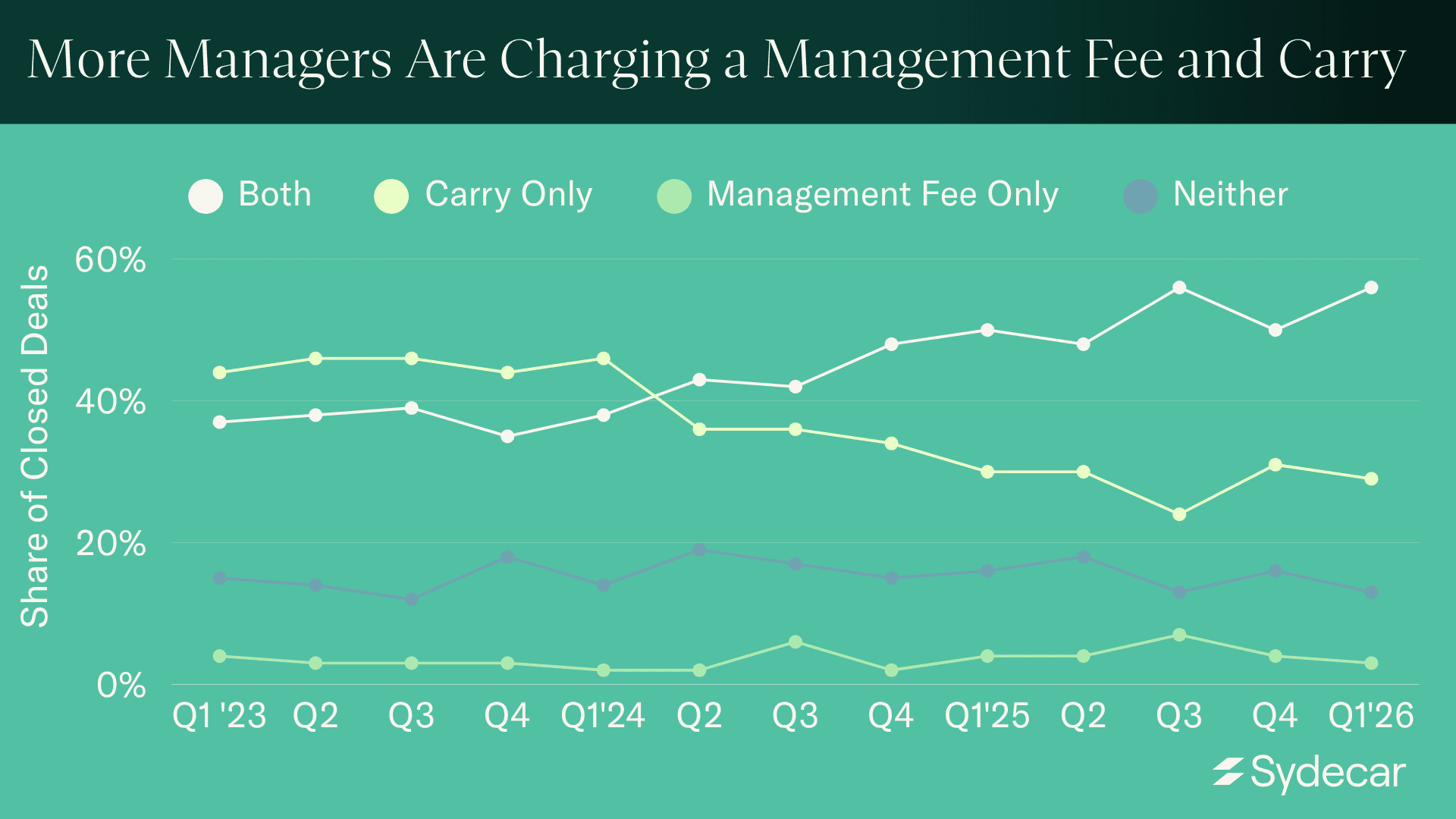

The data shows that managers are increasingly charging both carried interest and a management fee: the share of deals with both carry and a management fee has grown by more than 50% over the last three years.

This report analyzes fee structure data from nearly 4,000 closed SPVs on Sydecar's platform between Q1 2023 and Q1 2026. It breaks down how adoption of carry and management fees has shifted over those three years, how fee structures vary by raise size and investment stage, and what this data means for managers setting terms for their next deal.

More Managers Are Charging a Management Fee and Carry

Managers are not replacing carry with management fees. The share of deals charging carry has remained roughly flat, hovering at around 80% of all deals every quarter since Q1 2023.

Instead, managers are moving towards double-fee structures. Three years ago, SPV managers were most likely to charge carry only on their deals. In Q1 2023, 44% of deals charged carry with no management fee, while 37% charged both carry and a management fee.

That balance has shifted: in Q1 2026, 56% of SPVs charged both carry and a management fee. Carry-only deals dropped to 29%.

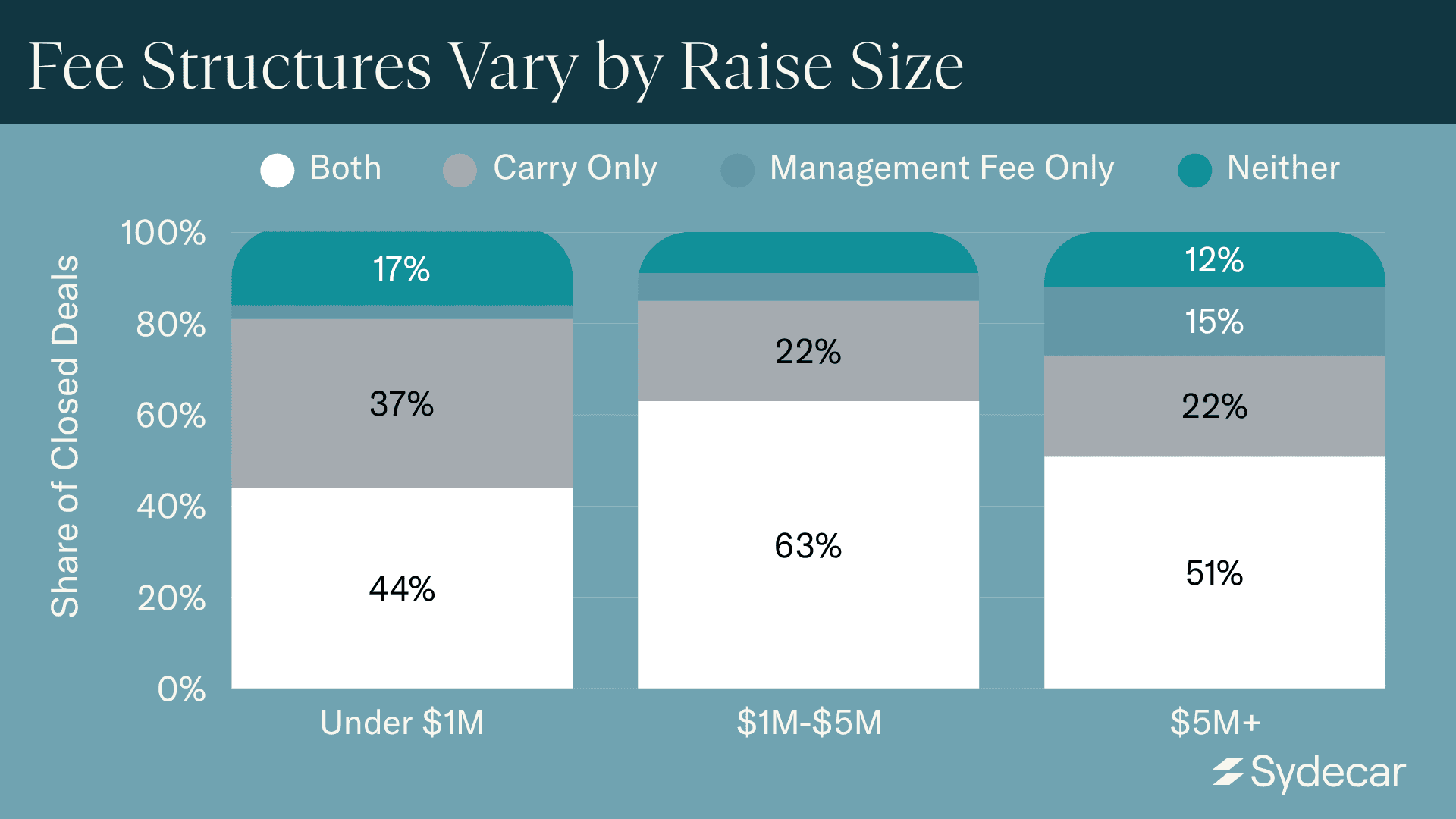

Fee Structures Vary by Raise Size

How a manager structures fees depends on deal size. The data show a clear pattern across three raise tiers: as deal size increases, the percentage of managers who charge both carry and a management fee increases, while the portion of managers who charge carry only decreases.

Carry most closely aligns the manager's incentives with the company and its investors. The manager is more likely to believe in and work harder for the company's success because the manager is paid only if the investment succeeds. A management fee, which is paid regardless of outcome, requires a higher level of established credibility to justify. Managers running larger deals tend to have a stronger track record, which makes it easier to charge both.

On the other hand, smaller deals are more likely to be run by new managers who may waive carry and/or management fees entirely as a gesture of good faith, to build their track record, and attract investors. Additionally, for raises below a certain size, charging these fees may not be worth the friction for the manager, particularly if the LP base is small and/or relationship-driven.

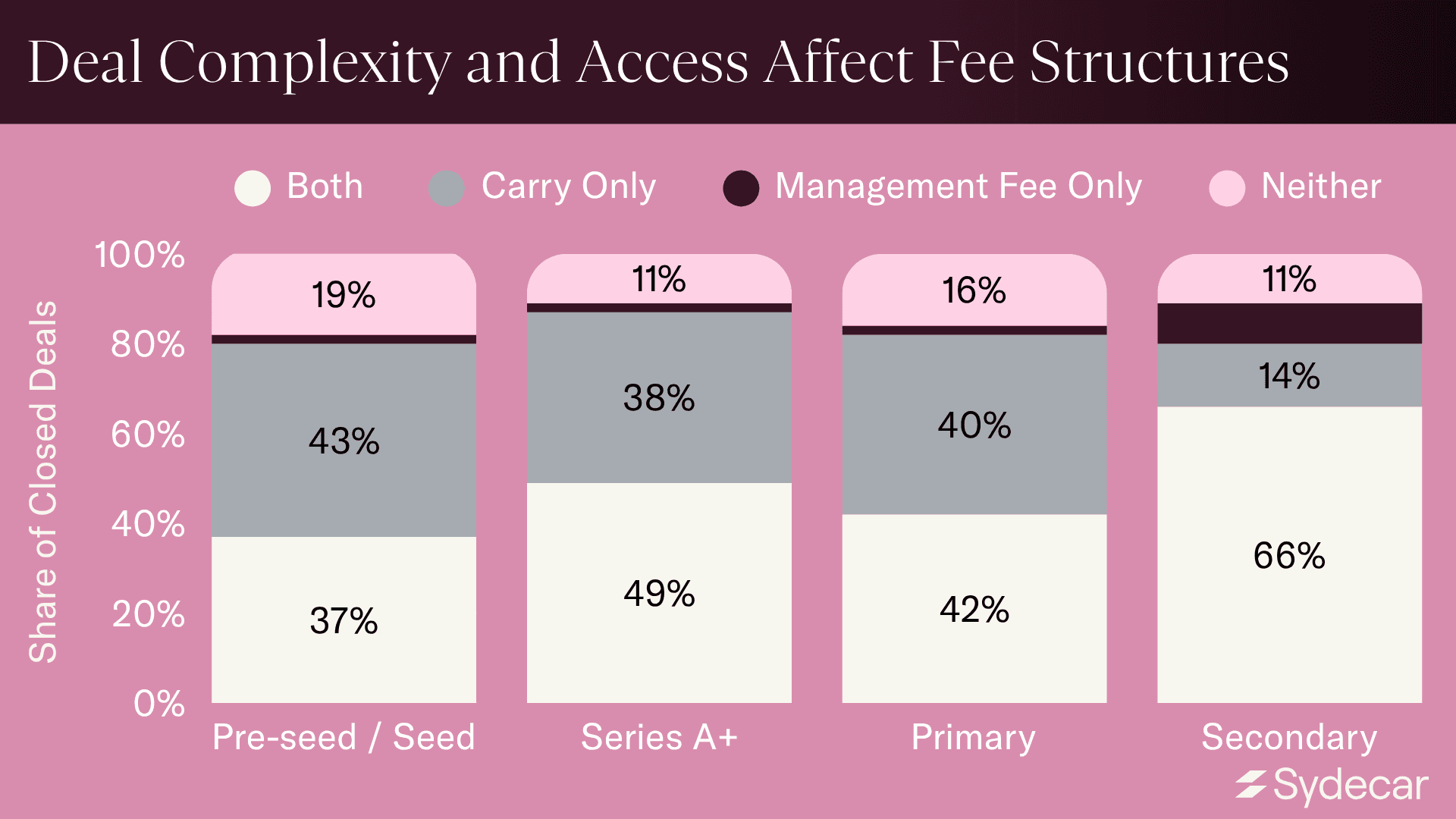

Deal Complexity and Access Affect Fee Structures

Fee structures also differ significantly by deal stage and deal type.

Early-stage (pre-seed/seed) deals are one-third less likely than later-stage deals to charge both carry and a management fee, and nearly twice as likely to charge neither.

Late-stage (Series A+) deals are harder to source and more competitive to win. Managers who gain access to a late-stage company are often getting into a deal that most investors cannot access directly. That scarcity justifies charging a management fee on top of carry. Late-stage deals are also typically more complex to source and structure and can require heightened diligence, negotiation, and coordination, giving managers a reasonable basis to ask investors to cover expenses and time through a management fee.

The investor profile in later-stage deals reinforces this pattern. Series A+ deals have a median check size that is 128% larger than that of pre-seed and seed-stage deals. Investors writing larger checks tend to be more sophisticated and more accustomed to carry and management fee terms, which helps explain why charging both carry and a management fee becomes increasingly common as stage increases.

Secondary deals work similarly. Among secondary SPVs, 66% charge both carry and a management fee, compared to 42% of primary deals. Carry-only structures are rare in secondaries; only 14% of secondary managers charge carry with no management fee, versus 40% on primary deals. Secondary transactions tend to involve highly sought-after, hard-to-access companies where primary allocations are limited or unavailable. That scarcity justifies charging a management fee on top of carry. And because secondary transactions tend to involve more work than direct investments (e.g., sourcing a seller, agreeing on a price, and coordinating legal transfer), a management fee alongside carry is a natural part of the structure.