At a Glance

VC managers choose between concentrated portfolios with higher ownership per deal and diversified portfolios with more total shots on goal.

Concentrated strategies rely on a small number of high-conviction investments where a single strong exit can return the fund.

Diversified strategies focus on maximizing exposure to power law outcomes by spreading smaller checks across more companies.

Each approach has tradeoffs in risk, ownership, portfolio size, and how LPs assess a manager’s discipline and credibility.

The right model depends on fund size, deal flow, and a manager’s ability to add value, maintain pricing discipline, and explain the math to LPs.

Portfolio construction involves many decisions, but two stand out: how many companies managers should back and how much they should invest in each. Some managers take a concentrated approach, writing larger checks into fewer startups. Others diversify, investing smaller amounts across many to increase their odds of landing an outlier. Both paths can work, but each comes with different trade-offs in ownership, portfolio size, risk, and LP perception. In today’s Sydeletter, we dive into the pros and cons of each.

Concentrated Portfolios: Depth Over Breadth

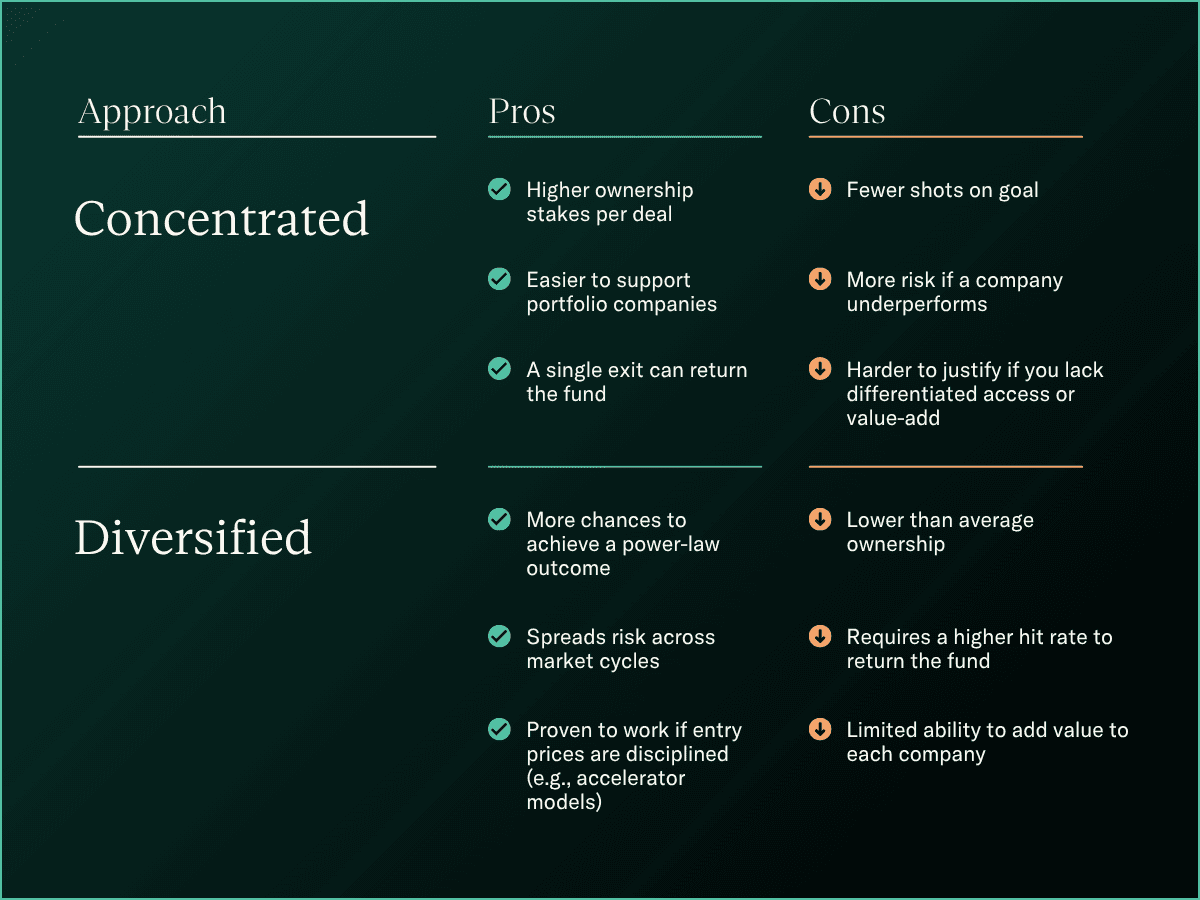

A concentrated approach means backing a smaller number of companies with larger checks and clear ownership targets. The math is simple but powerful: a single exit can return an entire small fund if ownership is meaningful.

Many managers choose this approach to stay focused and add hands-on value to each company, whether through close founder support, sharper governance, or hands-on guidance. With fewer portfolio companies, there’s room to go deep.

Concentration also enforces discipline. A clear portfolio model keeps managers from chasing deals outside their strategy. It also sharpens how managers define “winning”: not by logos or headlines, but by whether an exit can realistically return the fund.

At the same time, concentration doesn’t mean rigidity. Many emerging managers reserve a small portion of capital for outlier bets or raise SPVs to double down on breakout winners without disrupting their core strategy. Across Fund Is on Sydecar, most follow-on investments happen outside the fund through SPVs rather than from fund reserves.

The trade-off, however, is that fewer companies mean fewer opportunities to score. If ownership targets aren’t met or a core investment underperforms, the fund has less margin for error. Concentration raises the stakes on each decision.

Diversification: More Shots On Goal

On the other end of the spectrum, some managers spread capital across many companies, writing smaller checks with lower ownership. Accelerator models like 500 Startups show that when managers invest broadly but maintain consistent entry prices, the strategy can deliver strong results.

A “power-law outcome” refers to when one or two companies account for the majority of a portfolio’s returns. In a diversified strategy, the goal is to maximize exposure to potential outliers, knowing that most investments will underperform but a few can more than make up the difference. Diversification reduces dependency on any single company and spreads risk across market cycles. For managers with robust deal flow and strong networks, casting a wider net maximizes the likelihood of achieving a power-law outcome.

But this strategy comes with its own limits. Smaller checks and lower ownership make it harder for managers to add meaningful value to each company, and it often takes several strong outcomes to return the fund.

Beyond the math, there’s also an operational cost. Managing dozens (or even hundreds) of companies takes time and resources, from tracking performance to maintaining founder relationships. The broader the portfolio, the harder it becomes to stay engaged at the company level.

Pros & Cons at a Glance

Where Most Managers Land

There’s no universal “right” answer. What matters most is showing LPs that you’ve done the math and tied your approach to your fund size. A concentrated strategy highlights conviction and discipline. A diversified methodology maximizes exposure to power-law outcomes when paired with consistent entry prices. Either way, portfolio construction is as much about credibility with LPs as it is about fund returns.

If you want to see how this plays out in practice, our Data-Driven Guide to Portfolio Construction shares where Fund I managers actually fall on the spectrum from concentrated to spray & pray, along with benchmarks on average valuations by stage, initial vs. follow-on allocation, and more.