Introduction

The median fundraising time for SPVs on Sydecar is 28 days from launch to wire. However, that timeline can be much shorter or longer depending on various factors, some of which the SPV manager can influence, while others are constraints built into the deal itself.

This report analyzes average SPV fundraising timelines from thousands of deals across Sydecar's platform between 2023-2025, broken down by deal structure, raise size, LP count, investment round, sector, and manager experience. It gives managers a clear view of what drives fundraising speed, which factors they can influence, and realistic benchmarks they can compare themselves against.

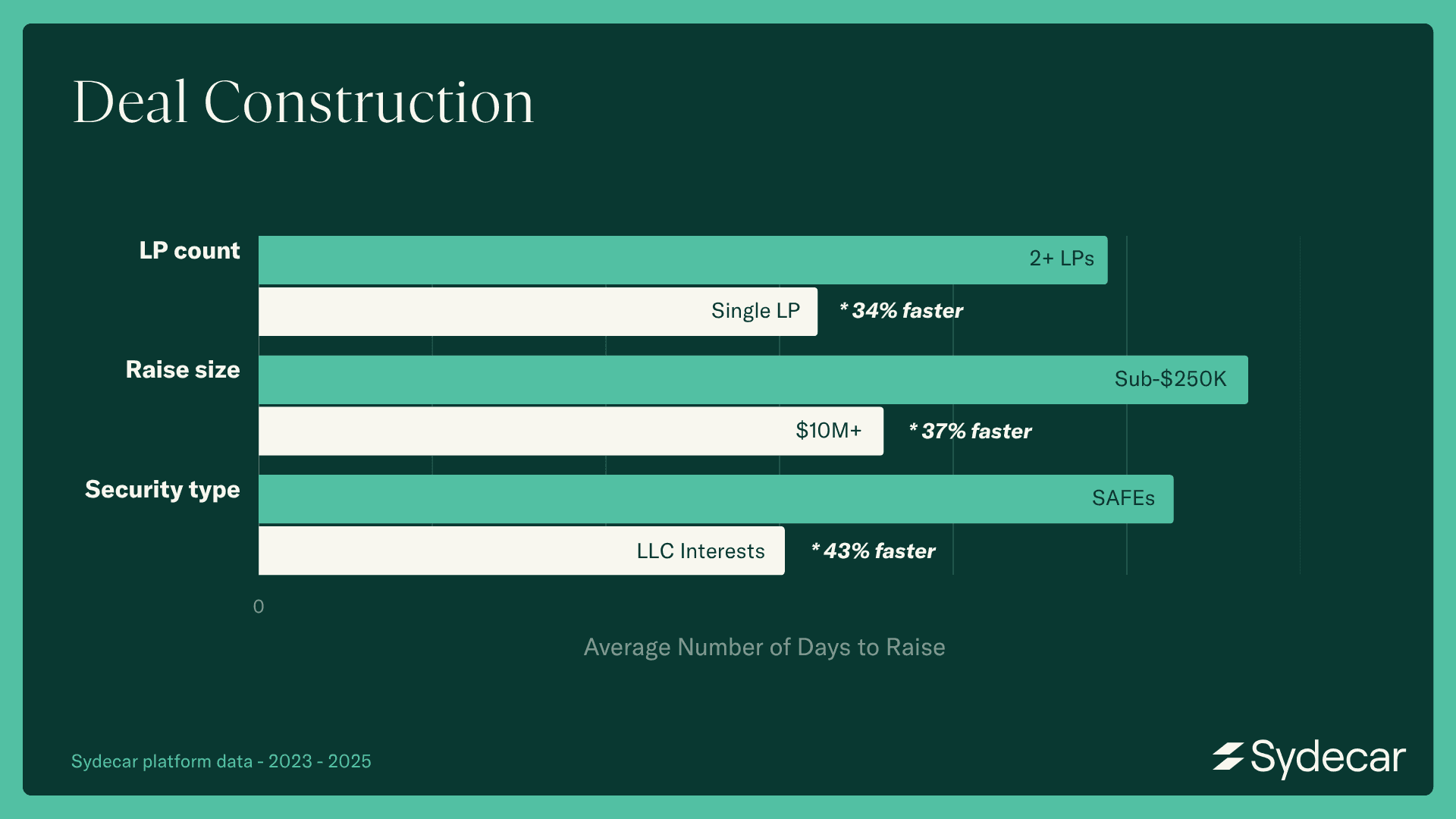

Deal Construction

SPV managers can control some of the biggest drivers of fundraising timelines, including security type, deal size, and LP count.

SPVs formed to purchase LLC interests close 43% faster than SAFEs on average. LLC interest deals tend to involve pre-secured allocations in high-demand, late-stage companies; these are situations where direct access to the investment likely was not available, and the allocation is already committed to a separate vehicle. That creates a built-in deadline: the SPV has to close within the target investment’s timeline, or it risks losing access to the deal entirely. Conversely, SAFEs are more commonly used for earlier-stage investments, where the allocation is less likely to disappear and LPs have more time to make their investment decision.

Raise size and fundraising speed move together. The larger the raise, the faster it tends to go. SPVs raising $10M or more close 37% faster on average than those under $250K. Similar to LLC interests, deal sizes greater than $10M tend to represent late-stage, high-demand companies. This speeds up fundraising timelines for two reasons: first, LP conviction is stronger in these deals, meaning they require less time to make an investment decision. Second, demand for these deals is higher, so the window to participate is shorter and more competitive.

LP count can also be linked to fundraising speed. Single-LP deals raise 34% faster than deals with multiple LPs. Single-LP deals are likely structured as anchor-led deals, in which terms are pre-agreed before fundraising begins, significantly reducing the fundraising timeline. On the other hand, in deals with more than 1 LP, each additional LP adds back-and-forth communication, additional documentation, and more coordination time.

All three data points point to the same insight: how long an SPV takes to raise is largely within the manager’s control.

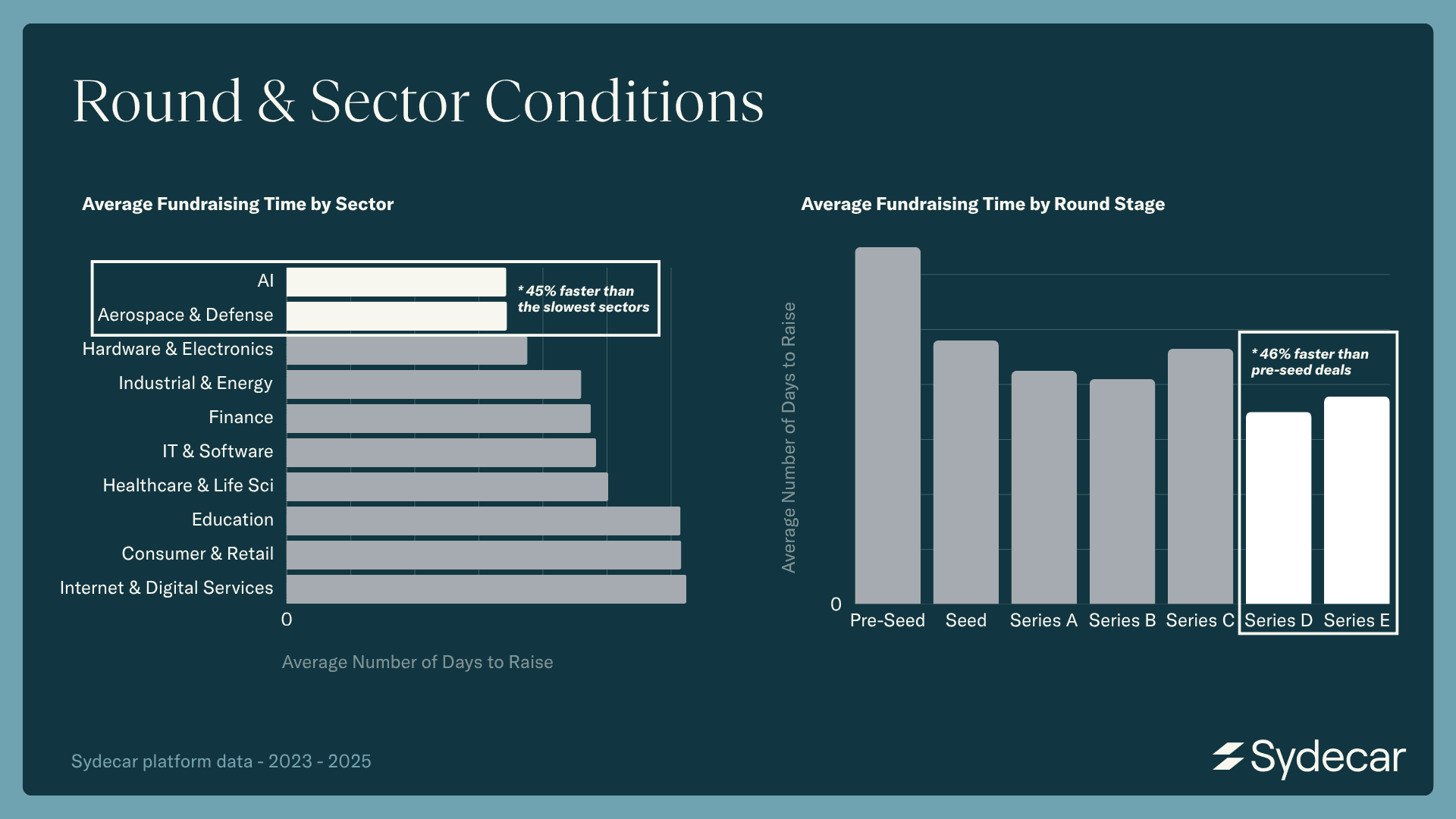

Round and Sector Conditions

However, not all factors that drive fundraising speed are within the manager's control. The company's funding stage and the sector it operates in affect fundraising timelines, regardless of how well the manager runs the process.

Series D+ deals raise 46% faster than pre-seed deals. In earlier-stage companies, LPs have less information to evaluate. There is less revenue, less traction, fewer customers, and fewer external signals that build confidence. By Series D+, the company’s track record gives LPs much more to work with, so decisions tend to happen faster.

Company sector also has a noticeable effect on fundraising timeline. The fastest sectors on the platform — AI and Aerospace & Defense — raise capital 45% faster than the slowest sectors: Consumer & Retail, Internet & Digital Services, and Education. A big part of that gap comes down to LP demand. AI is the most highly sought-after industry in venture right now, and defense tech has seen a surge in interest as geopolitical tensions and defense budgets have grown. LPs in those sectors already want in, which means less back-and-forth communication and faster decisions.

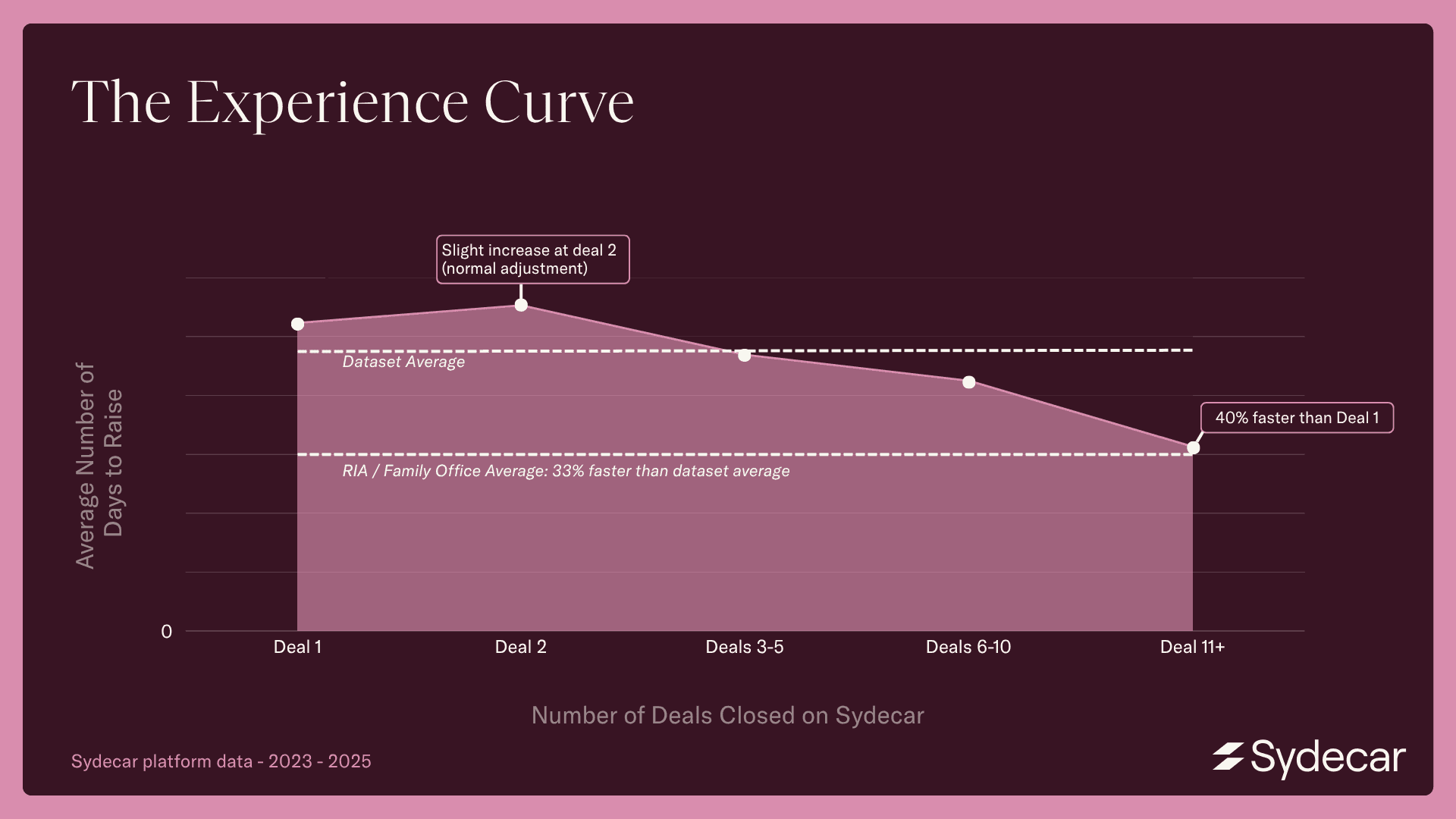

The Experience Curve

Close times get shorter with each deal a manager does on Sydecar’s platform. Managers on their 11th deal or later close 40% faster than they did on their first deal.

However, the path is not linear. Managers on their second deal average a slightly longer time to close than those on their first deal, but times consistently improve from their third deal onward. After a first close, managers may tweak how they pick LPs or structure their second deal in ways that create short-term friction. The data suggest this is a normal adjustment, rather than a regression.

Institutional investors, including RIAs and family offices, close deals 33% faster than the overall dataset average, and 27% faster than emerging fund managers. The faster speed comes from greater LP conviction, capital lined up in advance, and more deals under their belt.

What This Means for You

Some of the biggest drivers of fundraising speed are within your control. How you structure a deal, what security type you use, and how many LPs you bring in all have a measurable effect on how long your raise takes, and all of them are decisions you make before launch.

On the other hand, the company's stage and the sector you invest in set a baseline that exists independently of how well you run the process. A manager raising a pre-seed Consumer & Retail deal is likely going to experience a much longer fundraising timeline than the platform median. Simply knowing that changes how you should benchmark your own performance and how you communicate with your LPs.

And some of the speed simply comes with experience. The more deals you close, the faster you become, and the data shows that the fundraising timelines shrink exponentially over time.

Regardless, a manager who is deliberate about structure, selective about their LP base, and treats each raise as a learning for the next one will get faster over time. Most of what separates fast fundraisers from slow ones comes down to decisions, not circumstances.