At a Glance

Deal-by-deal investing through SPVs allows emerging managers to build track records, stay flexible, and gain exposure to top-tier deals without launching a fund.

SPVs help shift the focus from selling yourself to selling the opportunity, which can be more effective for newer GPs.

Syndicate leads add value by sourcing high-quality deals, bringing in strong co-investors, and building trust through transparent communication with LPs.

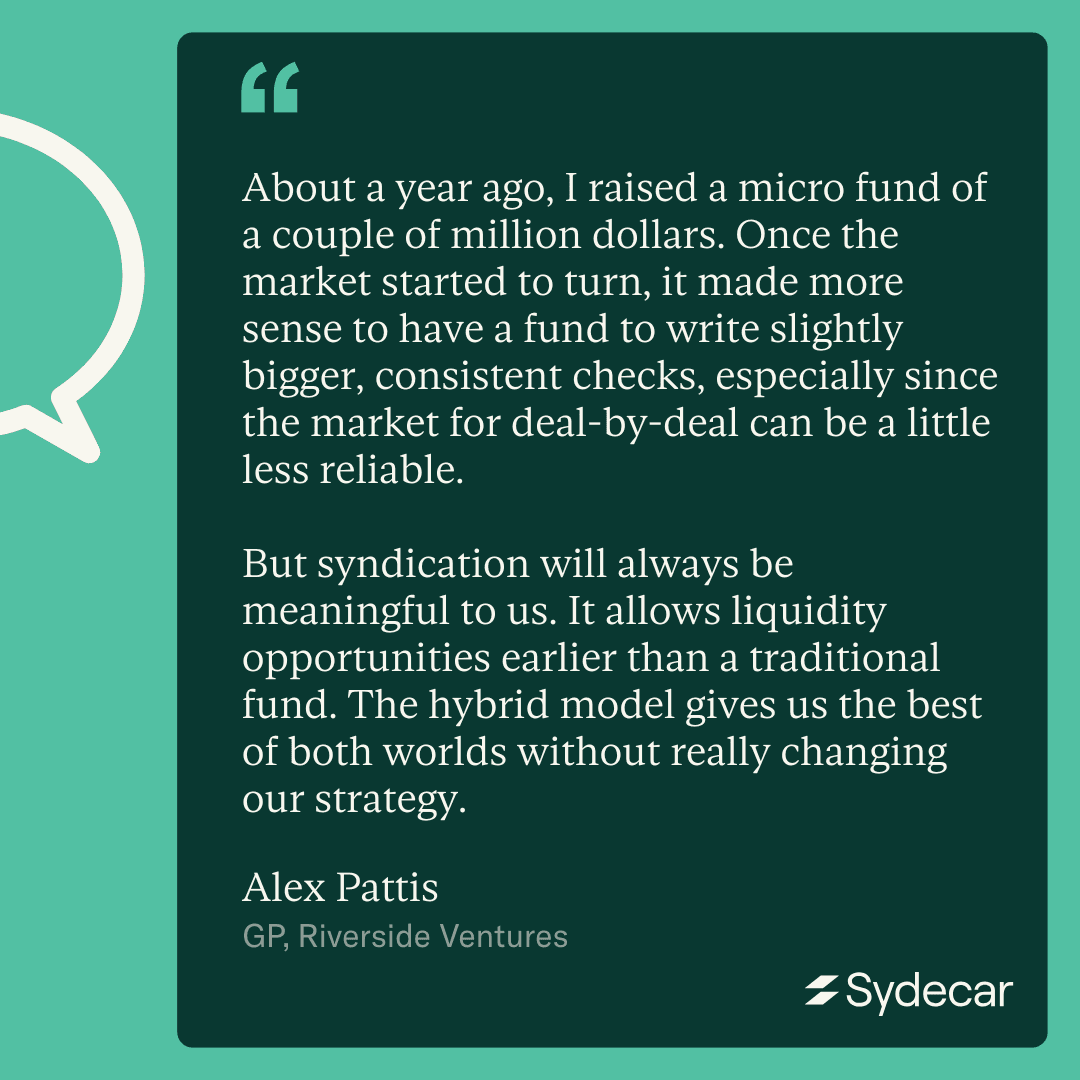

Many managers are layering committed capital funds on top of their syndicates, creating hybrid strategies that combine speed, control, and liquidity.

In venture capital, syndication refers to pooling capital from individual angel investors or venture firms to invest in a private company via a single check. Syndicate members often collaborate on deal sourcing, diligence, and portfolio support.

Syndicates are in many ways the lifeblood of early-stage VC. They increase access to venture investing for both investors and deal managers. They also increase access to capital for early-stage founders.

Deal-by-deal investing is more than just a way for influencers to monetize their audience or for retail investors to get $1k checks into hot deals. A deal-by-deal investing strategy, on its own or alongside a committed capital fund, can make a manager more attractive to LPs, more valuable to founders, and more flexible in how they can deploy capital.

Managing a syndicate was once seen as just a stepping stone–a way to build a track record with the hope of one day being taken seriously as an investor. Today, however, they are recognized as durable strategies that create meaningful value for their founders, their LPs, and themselves.

Alex Pattis and Zach Ginsburg have extensive experience navigating the landscape of deal-by-deal investing. Since launching Riverside Ventures (Alex) and Calm Ventures (Zach), the two syndicate managers have collectively deployed hundreds of millions of dollars into hundreds of startups, largely through SPVs.

Together, they author Last Money In, the most actionable newsletter in venture capital. We sat down with Alex and Zach to better understand the role that deal-by-deal investing plays in the venture capital ecosystem.

Key Takeaways

Your Syndicate is Your Deal Flow: Simply launching a syndicate isn’t enough to build a compelling track record. Consider how you can use your syndicate as a source of deal flow to share with established managers as you build your network. If you want to eventually graduate to managing a fund, the relationship you built while syndicating deals could be invaluable.

Be a Super-Connector: Bringing established managers into deals can help you earn or increase your allocation to an exciting company. Being a super-connector also increases your value to founders, allowing you to contribute to their hiring, sales, and business development efforts.

Build Trust Through Communication: When raising a fund, you are selling yourself and your strategy to LPs. When raising for SPVs, you are constantly selling an opportunity, traction, and the story behind a company. Understand what resonates with your LPs and communicate with them transparently.

Operationalize Your Workflows: Deal-by-deal investing offers more flexibility. More flexibility gives you more options, allowing you to invest across any sector, stage, or geography. With more opportunities for distraction, streamlining your workflows and building repeatable processes are key to running a successful syndicate.

Selling Yourself vs. Selling the Opportunity

Raising capital for an SPV requires selling investors on the founder, their company, its traction, and its growth story. An investor’s attention is focused on the opportunity itself, rather than these deal managers. What does the company do? What type of traction does it have? Who are the other investors involved? These are all questions potential LPs may ask before making their own investment decision.

Traditional funds are all about the manager, their network, and their strategy. What is the manager’s background? What investments have they made in the past? What is their overarching thesis? These are good questions for a potential LP to ask a fundraising manager, but they may be hard to answer if you’re just getting started.

SPVs allow an investor early in their career to focus LP attention on the opportunity itself rather than exposing any vulnerabilities in their own track record (or lack thereof).

Your Value is Your Deal Flow

The best way to get started with SPVs is to be a strong source of deal flow for other established investors. By helping other investors in the ecosystem, you can build your own deal flow and access better deals.

LPs are often hesitant to get involved in a syndicated deal until there is a strong lead investor. But it’s hard to get allocation once there’s a strong lead investor in a deal. The best way to stay ahead of this curve is to become the person who brings a strong lead into a round.

This builds your credibility with established funds, cements your reputation as a strong source of deal flow, and demonstrates your value to other founders.

Becoming a deal-flow superconnector can be challenging. While deal-by-deal investing does allow you to build a track record quickly, there’s no shortcut to the hard work of finding exciting founders to invest in before everybody else. However, this type of work compounds. Once your network is established, you’ll find that deals come to you with little effort.

One quality that remains consistent is the role of syndicate leads as super-connectors. Whether you’re connecting a founder to a VC, an LP to another syndicate, or two LPs to each other, the role of syndicate leads as facilitators in the ecosystem is a big part of their value.

Leveling Up: The Path of a Successful Syndicate Manager

It’s well understood that deal-by-deal investing can be an efficient way for an aspiring VC to build a track record. What’s less understood is what happens once you’ve demonstrated success as a syndicate manager (in the form of distributions or significant markups).

At this point, many syndicate leads find themselves drawn to raising a committed capital fund so they can spend less time fundraising, move more quickly on hot deals, and focus on their portfolio construction strategy.

Alex Pattis and Zach Ginsburg have both “graduated” to managing their own funds, but that doesn’t mean that they’ve left deal-by-deal investing aside. Instead, they’ve layered on committed capital in a hybrid approach to venture investing.

A hybrid model is a structure in which a manager operates both a committed capital fund and a syndicate. In this model, the fund can lead the process, commit capital to a founder, and then open up additional allocation to LPs. This is also referred to as providing “co-invest” opportunities to LPs.

Learn more about how to use Co-Investing as a Competitive Advantage.

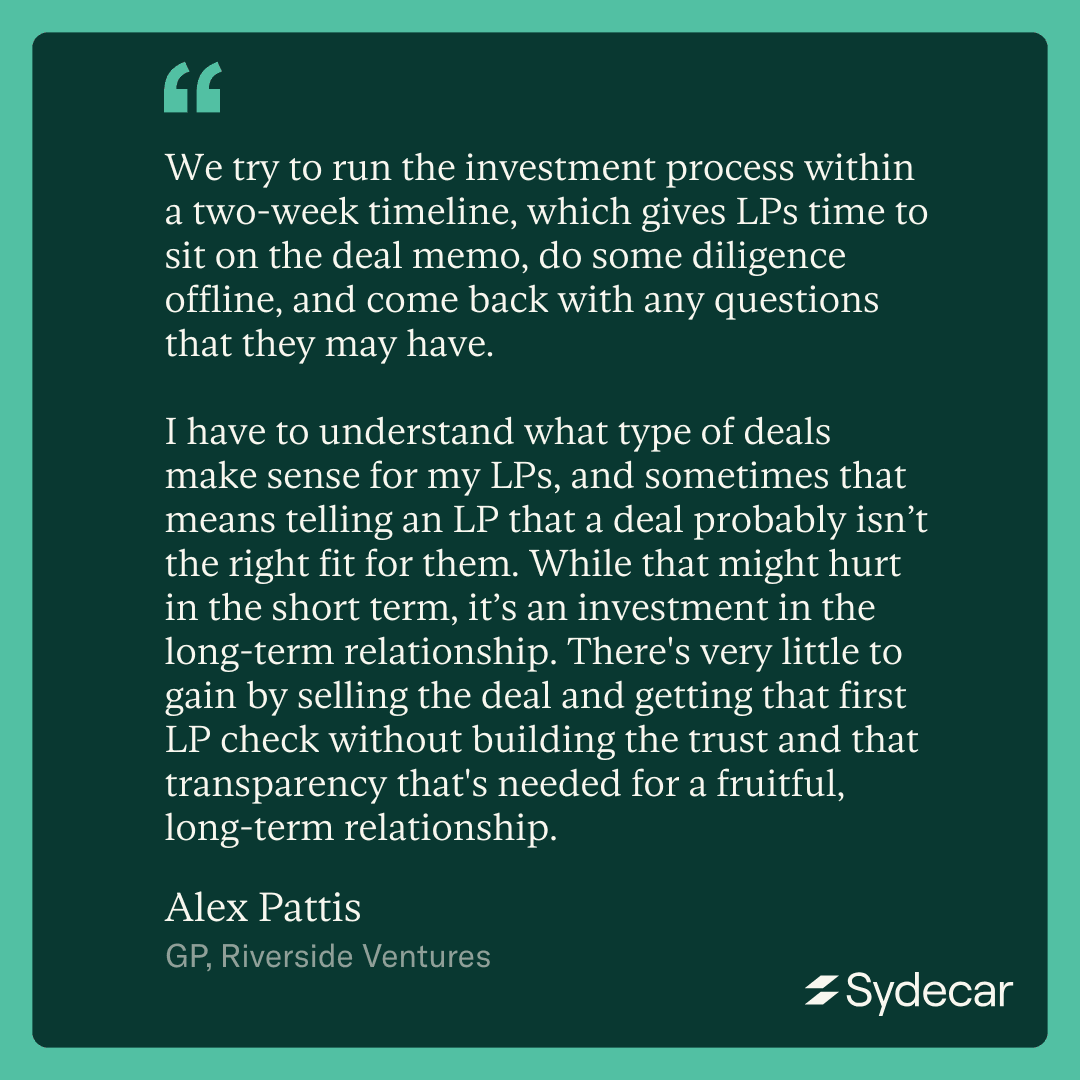

Undertaking a hybrid model can reveal vulnerabilities in your operational processes that are easy to ignore when your deals are infrequent or your investor base is smaller. Hybrid managers like Alex and Zach have found that proactive, clear communication with all stakeholders is key to a smooth investment process.

Establishing clear and reliable channels of communication with LPs is key to building trust. In practice, this means putting in the time to draft comprehensive deal memos and then making yourself available to answer ad hoc questions relatively quickly.

Rather than hard-selling the deal, focus on what you know about your LPs. Not every deal will be the right fit for every LP, and it’s important to present the opportunity as it is rather than embellishing. Any exaggerations are short-sighted in a relationship that should be long-term with LPs.

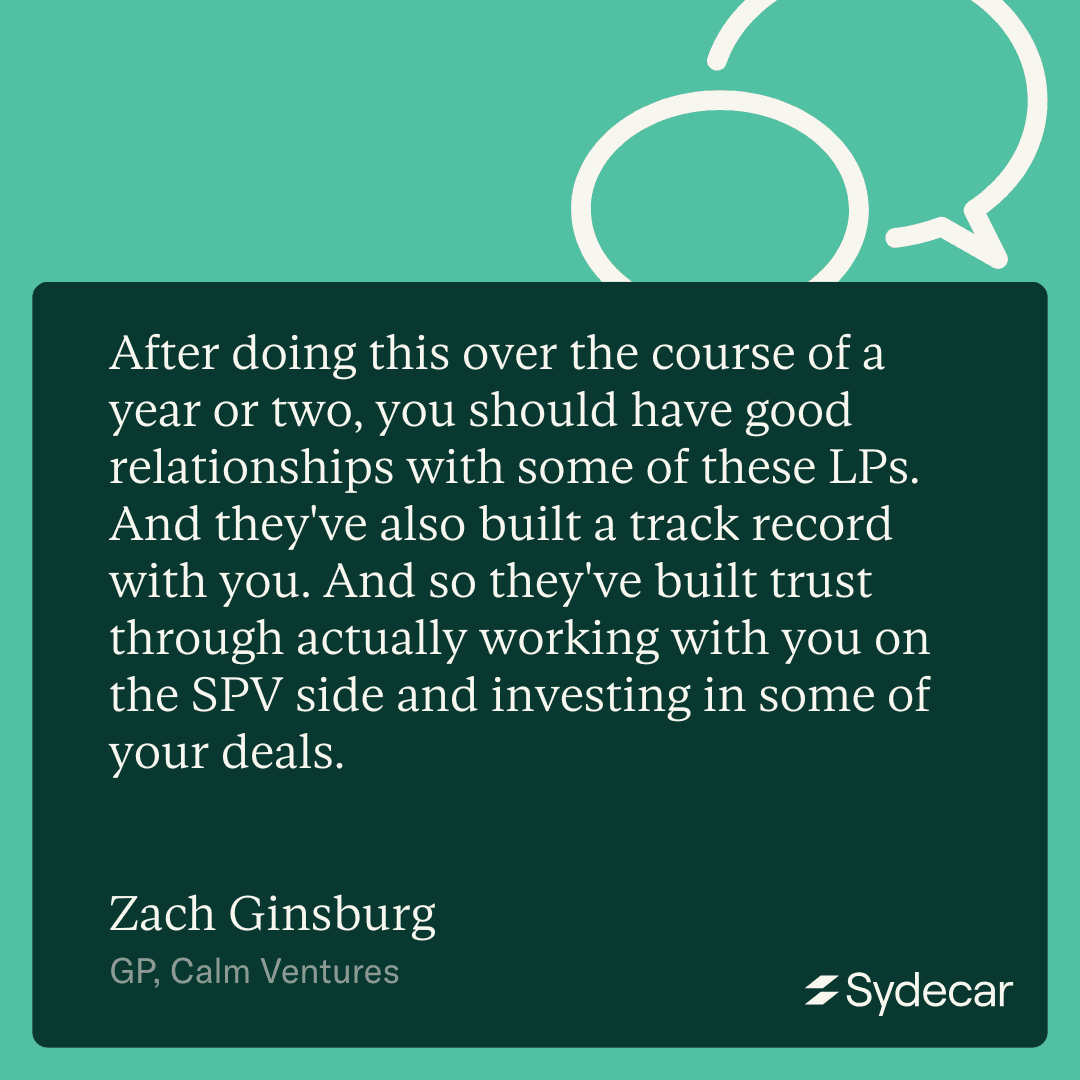

These relationships take a long time to build, so deal-by-deal investing is a good way to build trust with LPs. Some of Alex and Zach’s LPs have been with them for many years and have seen hundreds of deal memos.

Not only do LPs get to evaluate the deal themselves, they also evaluate Alex and Zach’s analysis of the deal. What does this GP think? Does it align with the way we go about deals? Showing investors how you think with each deal memo is an effective way to build that relationship over time.

Enjoyed the recap? Check out the full conversation here.

—

From formation and onboarding to compliance, tax, and reporting, Sydecar handles every operational detail in a single, integrated platform.

Our dedicated support team works behind the scenes as your operating partner, while our transparent, cost-effective pricing allows you to deploy more capital into deals, not administration. Sydecar delivers a streamlined, professional experience for you and your investors from day one.

If this piece has you thinking beyond one deal, our guide is the natural next read. Access The Comprehensive Playbook for Starting (and Running) a Syndicate for practical guidance on investor growth, SPV execution, and distributions.